Our Legal Blog

Your Resource For Legal Information

Trying to decide between a will and a trust in New York? Learn the key differences and how to choose the right estate planning tool for your needs.

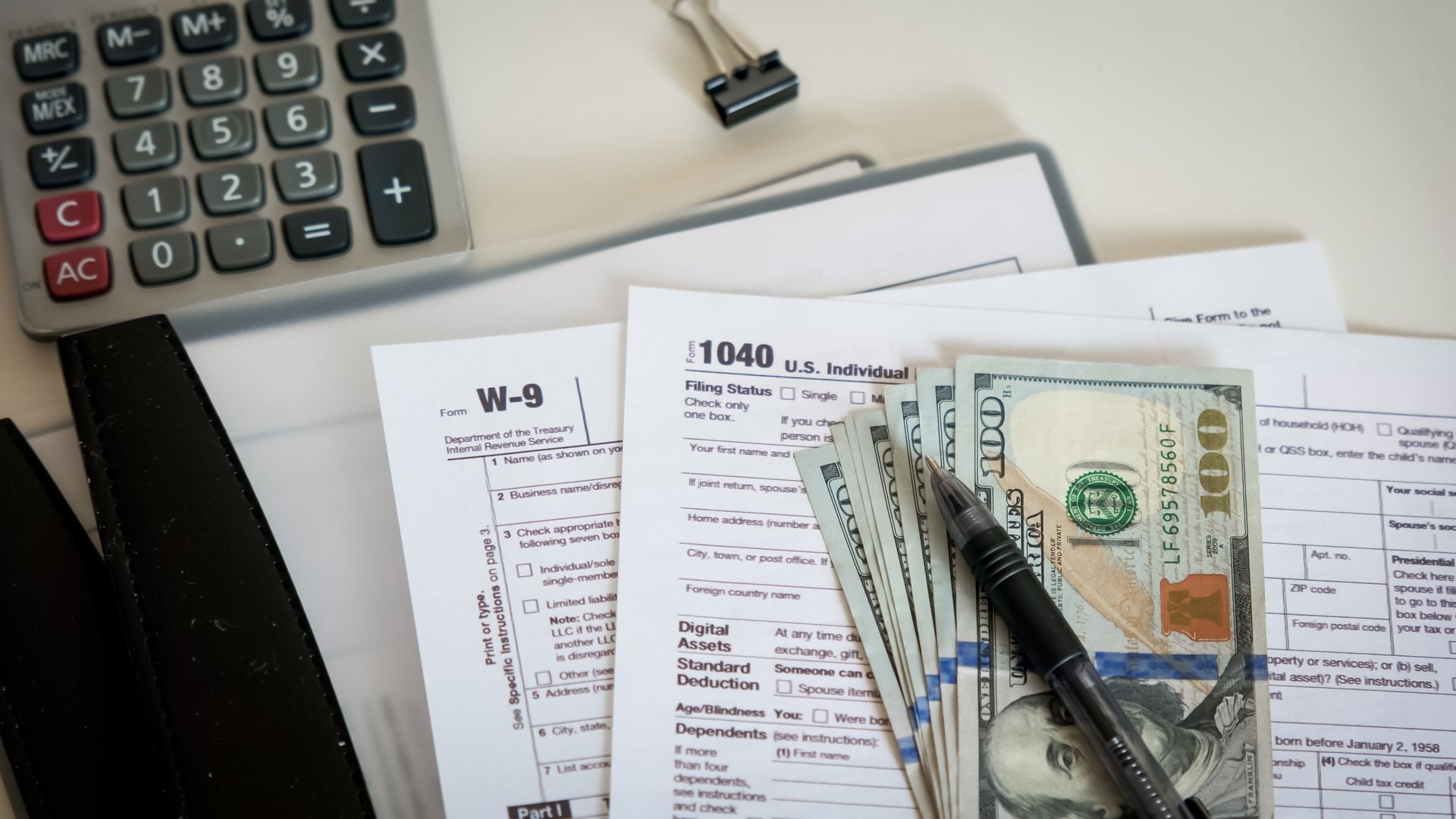

What to Do If You Receive an IRS Notice in New York

Choosing between an LLC and a corporation in New York? Learn the key differences, benefits, and which structure is best for your business.

Learn how trusts can protect assets during your lifetime, provide control, and support long-term planning. Discover how Auerbach Law Group, P.C. assists New York clients with trust planning. Call (212) 840-2180.

Learn the differences between business litigation and mediation, when each approach makes sense, and how Auerbach Law Group, P.C. helps New York businesses resolve disputes. Call (212) 840-2180 today.

Learn what happens after an IRS civil tax audit in New York, possible outcomes, next steps, and how Auerbach Law Group, P.C. can help protect your rights. Call (212) 840-2180 today.

Why Estate Planning Matters in New York: Wills, Trusts, and Peace of Mind

Resolving Business Disputes in New York: Why Legal Strategy Matters

How to Handle an IRS Audit: What You Should Know Before Responding

This is a subtitle for your new post